Let’s be honest—when it comes to managing your investments, you’ve probably asked yourself, “Do I really need an advisor?” After all, we live in a world where apps can help you invest with just a few clicks. Why pay someone else to do what you can easily do yourself, right? Well, hold that thought for a second. There’s a bit more to consider when deciding how to manage your financial future—especially when you start drawing from those funds in retirement.

THE CASE FOR GOING PASSIVE: LOW MAINTENANCE, HIGH PATIENCE

Many people find success in passive investing, and for good reason! It’s a bit like owning a well-behaved cat: you don’t have to walk it every day, and it rarely makes a mess. Passive investments, such as index funds or ETFs (Exchange-Traded Funds), simply track the performance of a market index, like the S&P 500, without requiring daily adjustments. The advantage? Low costs, broad diversification, and historically strong long-term growth.

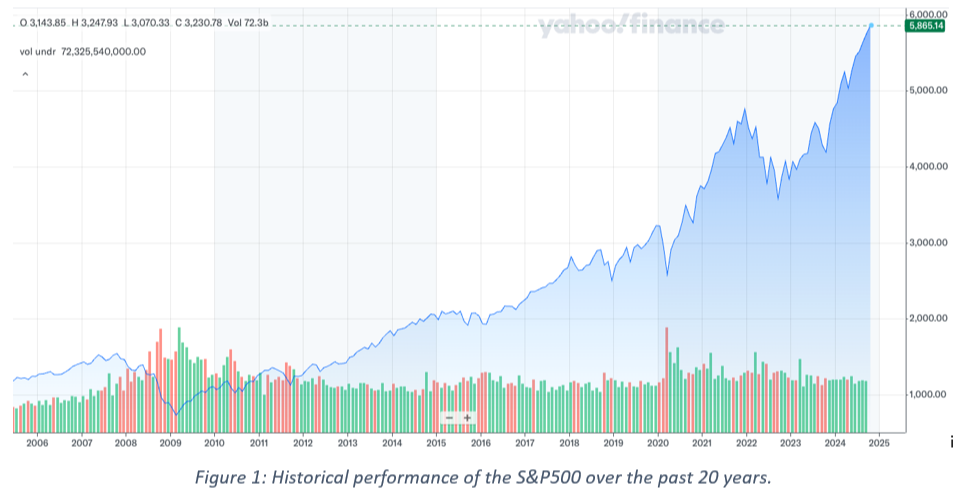

Take the S&P 500 as an example. Over the past few decades, despite recessions, booms, and busts, it’s delivered an average annual return of about 10%. Let’s imagine that 20 years ago, you invested $100,000 in the S&P500. Today, that investment would be worth over $700,000. Not too shabby for something that doesn’t require a lot of active management! This makes passive investing particularly attractive for people who are still accumulating wealth or have a long-time horizon.

SO WHY BOTHER WITH AN ADVISOR?

While passive investments strategies are great for the “set it and forget it” crowd, things get trickier when you’re nearing retirement—or, even more importantly, when you’re already retired and drawing from those accounts. At this stage, volatility matters more... a lot more. You’re no longer contributing to your portfolio; instead, you’re withdrawing funds to cover living expenses. If a market dip occurs right when you need money, it can significantly impact your retirement savings. That’s where an investment advisor, particularly one that specializes in retirement, comes in handy.

ENTER ACTIVE MANAGEMENT: THE "HANDS-ON" APPROACH

An investment advisor can recommend a more active investing strategy as you approach retirement. Consider the situation of a retiree during the 2008 Financial Crisis. Between late 2007 and early 2009, the US stock market experienced its worst decline ever, dropping by 50%. It then took 66 months for the market to recover.

This means that if you had a passive investment strategy and needed to withdraw money for your expenses during that time, you could have faced major losses, which might have jeopardized your financial plans. For instance, if you started with $1,000,000 and withdrew $100,000 a year, you would not have enough to cover five years’ worth of income. Granted, this is a very extreme scenario.

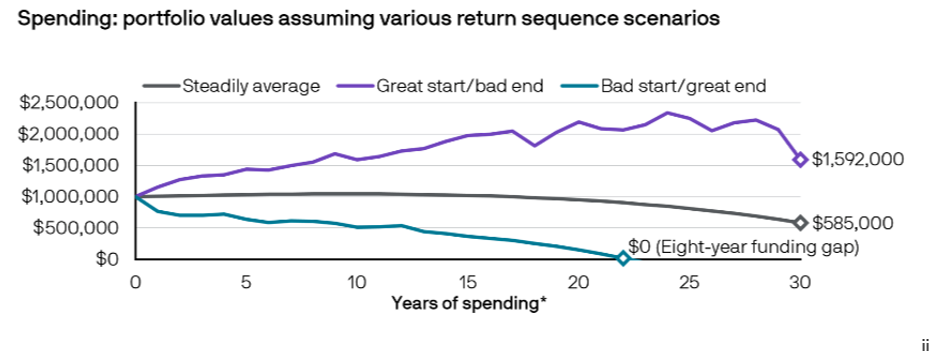

A more realistic example is illustrated below. This spending in retirement chart assumes an initial $1,000,000 and a 4% withdrawal, adjusted annually for inflation of 2.5%. In this example. The initial investment would provide income for less than 25 years.

In short, if you had a passive strategy and needed to withdraw funds for your expenses at that time, you might have locked in significant losses, potentially derailing your financial plan.

An advisor with an active management style, however, would have had strategies in place to mitigate that risk—like reallocating assets to safer investments, diversifying more broadly, or even using cash reserves to help weather the storm. In other words, they can offer personalized guidance and adjustments based on your specific needs, risk tolerance, and time horizon. They act like a financial co-pilot, ready to make course corrections when the market gets bumpy.

REAL-LIFE EXAMPLE: THE RETIREMENT RED ZONE

Let’s say you’re five years away from retirement—a time we call the “retirement red zone.” During this period, your financial decisions can have an outsized impact on the success of your retirement. An advisor might recommend shifting a portion of your portfolio into less volatile, income-generating investments. Historically, retirees who made these adjustments before events like the 2008 crash fared much better than those who didn’t. Having a personalized game plan can mean the difference between thriving and merely surviving.

CAN’T I JUST DO IT MYSELF?

Of course, you can do it yourself. Plenty of people have. But here’s the thing: managing your investments, especially in retirement, is a full-time job that requires a lot of experience and emotional discipline. The stock market is unpredictable, and it’s easy to make knee-jerk decisions when the market drops 10% in a week. An advisor brings experience, perspective, and a rational voice to help you stay on track. They also help with tax planning, rebalancing, and other aspects that can maximize your long-term success.

SO, DO YOU REALLY NEED AN INVESTMENT ADVISOR?

That’s a question only you can answer. But consider this: if you’re a seasoned DIY investor with a stomach of steel, passive investing might suit you just fine. If you’re approaching retirement or navigating complex financial situations, the value of an advisor becomes more obvious. They help ensure that your investments aren’t just growing but growing in alignment with your life goals.

In the end, the goal isn’t just to beat the market—it’s to achieve financial freedom and security. So, whether you choose passive investing or active management, just make sure your strategy suits your stage in life, and that it’s working for you.

CONCLUSION: BE THE PILOT, BUT KNOW WHEN TO ASK FOR A CO-PILOT

At the end of the day, financial success doesn’t come from just setting it and forgetting it or trying to outperform the market. It’s about creating a plan that works for your goals and your lifestyle. And sometimes, that means having a trusted advisor by your side to navigate the unexpected twists and turns along the way.

i Source: Yahoo Finance. "S&P 500 (^GSPC) Historical Price Chart Since 10/2004." Accessed October 15, 2024. Available at: https://finance.yahoo.com/quote/%5EGSPC. ii Source: J.P. Morgan Asset Management. "Guide to Retirement." Hypothetical return scenarios are for illustrative purposes only and are not meant to represent an actual asset allocation. Spending in retirement chart assumes an initial $1,000,000 and a 4% withdrawal adjusted annually for inflation of 2.5%. Available at: https://am.jpmorgan.com/us/en/asset-management/protected/adv/insights/retirement-insights/guide-to-retirement.